Mini-Strategics: Solving Medtech's Liquidity Design Problem

Hosting the State of Medtech podcast, I noticed a common theme as I interviewed founders, VCs, and strategics.

For years, medtech founders have been saying there’s a “funding problem.”

VCs have been saying there’s an “exit problem.”

And strategics… well, they don’t really like to go on record commenting on much — but given the fall in valuations, the acquire-and-conquest playbook of the last decade isn’t working the same way anymore.

It’s more precise to call it a liquidity design problem.

When there are few natural buyers and their roadmaps are crowded, exits slow, venture capital recycles more cautiously, and Seed/A rounds get rationed. That design is changing.

Strategic spin-outs are reconstituting the industry into a denser graph of focused acquirers.

Think GE HealthCare in imaging/monitoring, Solventum in wound/oral/filtration, and (newly announced) DePuy Synthes as an orthopedics pure play.

I call these Mini-Strategics — roughly $3–$15B revenue businesses that have the scale and one mandate: win their niche and compound.

What is a “Mini-Strategic”?

A Mini-Strategic is a mid-cap, pure-play healthcare company typically in the $3B to $15B revenue range — that has emerged from a corporate spin-out, carve-out, or targeted divestiture.

It retains the scale, channels, and brand equity of its former parent, but operates with: focused governance, dedicated capital, a singular market mandate.

They typically launch with billions in revenue, specialist investors, and a single-segment story. Some notable examples of this:

- Solventum (3M Health Care spin, 2024) posted $8.2B 2023 sales across Medical Surgical, Dental, Health Information Systems, and Purification & Filtration — now explicitly guiding to bolt-on acquisitions.

- DePuy Synthes (J&J orthopedics) is now planned to be separated within 18–24 months, a $9.2B franchise refocused to compete head-on in trauma, recon, and extremities.

- GE HealthCare (spun 2023) focuses on Imaging, Ultrasound, Patient Care Solutions, and Pharma Diagnostics — with its own M&A currency and a >$1B R&D engine.

- Vantive (Baxter kidney care) will stand up under Carlyle via a $3.8B sale, creating a consolidation platform in renal care.

- Other examples: ZimVie (spine/dental from ZB, 2022), VB Spine (Stryker spine division), Embecta (diabetes injection from BD, 2022), Varex (x-ray components from Varian, 2017).

Two structural advantages power the Mini-Strategic

Dedicated Capital Allocation: Freed from competing internally against high-growth divisions (like robotics or advanced interventional cardiology) for the parent company’s R&D and acquisition budget, the Mini-Strategic can allocate capital solely toward its specific business objectives.

Clear Market Narrative: The new entity attracts specialized investors who value stability and consistent growth in a specific vertical (e.g., orthopedics or wound care), justifying a valuation multiple often superior to the discounted valuation the segment received within the diversified conglomerate. (e.g., Danaher/Veralto logic; J&J’s post-Kenvue focus.)

Why competition gets healthier (and faster)

1) Focused pressure → faster external innovation

Inside a behemoth such as J&J, an ortho division like DePuy can get optimized for internal efficiency.

Unfortunately, it also gets compared to the rest of the portfolio — like fast-growing interventional cardiology or cash-rich pharma.

As a standalone, DePuy Synthes must win share directly against Stryker and Medtronic, with M&A as a primary avenue — not just a consideration.

Likewise, Solventum must move wound/oral/filtration forward; it can’t hide in a 3M slide.

That urgency re-weights the classic “build vs. buy” calculation toward complementary M&A with startups — especially those with regulatory assets and evidence packages ready to slot into established channels.

2) More — and better-matched — buyers

The buyer universe expands beyond a handful of traditional strategics like Medtronic, Boston Scientific, J&J, Stryker, and Abbott.

You now have Mini-Strategics with explicit mandates and PE platforms executing buy-and-build (e.g., Carlyle’s Vantive).

PE creates a platform, optimizes operations, bolts on sub-$200M startups, and later IPOs or sells to a larger strategic.

More credible suitors = higher probability and speed of exit.

Reality check: divestment paths are market-sensitive. Medtronic explored spinning/selling Patient Monitoring & Respiratory Interventions to PE in 2023, then chose to retain, rebrand, and restructure the business in 2024 — a reminder that spin vs. stay can change with performance and markets.

The virtuous cycle: Exits → Liquidity → Early-stage risk

HSBC’s H1-2025 venture report shows a familiar pattern: more dollars, roughly flat deal counts — capital concentrating in later stages and fewer first financings.

In parallel, our This Month in Medtech series on State of Medtech (via LSI Compass) highlights the same arc inside devices: consolidation and concentration.

That means capital, M&A, and innovation are clustering around proven technologies and commercial-stage players.

Early-stage checks are tighter; mid-to-late-stage companies with clear market validation are commanding premium valuations.

If you’re a founder raising money, don’t stop reading. It gets better for you…

This pattern rarely reverses on sentiment. It reverses when distributions restart and LPs feel safe recycling into Seed and Series A.

That’s exactly where Mini-Strategics (spin-outs and PE carve-outs) matter:

More focused buyers → more repeatable M&A → faster distributions → earlier risk gets funded again.

When exits happen in shorter windows — and we see more corporate-led rounds — confidence returns to fund medtech because there’s a clear path to liquidity.

As large, repeatable exits resume, enabled by the dual buyer pool (Mini-Strategics + PE platforms vs. Traditional Strategics) — funds can recycle into earlier, riskier ideas again.

Liquidity begets risk-taking.

Simultaneously, industry analysts (EY, McKinsey) argue that medtech needs portfolio moves and operating-model focus to reignite Total Shareholder Return — exactly what spin-outs catalyze.

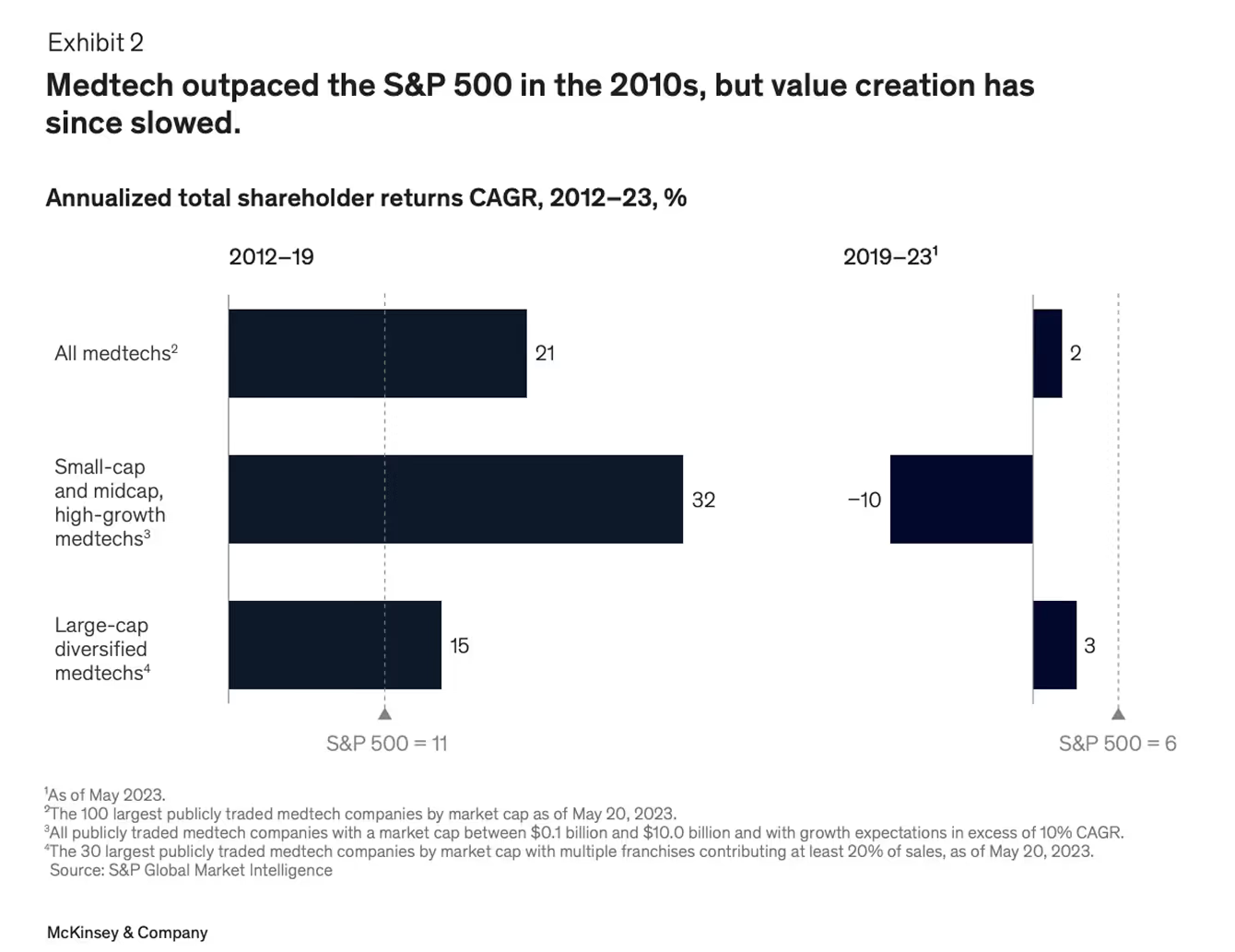

McKinsey’sMedtech Pulse from 2023 shows this chart which might be a shock to many given how hard the last few years has been.

The single biggest reason medtech’s value creation has cooled isn’t cost or regulation—it’s focus

When capital was trapped inside huge, sprawling portfolios, every division became “average.”

The industry’s innovation engine diluted.

Mini-Strategics are the antidote: smaller, purer, and structurally designed to make bold bets again.

More importantly, they restore focus and rebuild the innovation-margin loop that once powered medtech’s outperformance.

But lets get back to a bigger picture quote I highlighted earlier; Liquidity begets risk-taking.

Liquidity begets risk-taking (and why medtech needs it)

When capital is abundant, founders don’t merely raise larger rounds; the whole system tolerates more shots on goal.

Recently I’ve been reading Boom: Bubbles and the End of Stagnation and the core mechanism behind innovation is:

- Vast Funding → Opportunity: Surges of capital underwrite projects that would never pencil in “normal” times.

- Lowered Risk Aversion: With money moving fast, the perceived risk of not participating eclipses the risk of trying. FOMO and “definite optimism” coordinate mass experimentation.

- Over-Investment (by design): Yes, it overshoots. But the excess builds durable infrastructure and know-how that remain after the cycle cools.

Translate that to medtech: today’s concentration (more dollars into fewer later-stage names) constrains exactly this permission set.

Mini-Strategics are the practical fix — not by creating a bubble, but by manufacturing repeatable exits.

Distributions restart → GPs loosen their risk budget → Seed/A backs bolder device science again.

In other words, M&A liquidity is the socially acceptable version of “vast funding”: it keeps the experimentation engine running without needing an IPO boom.

If this cycle starts to take off, we will see an influx of capital and a potential “bubble” in medtech.

But I argue that’s what we need for innovation, bigger bets, and truly life-altering breakthroughs for patients.

“Liquidity is the mother of courage. When exits are possible, founders attempt the impossible — and someone will fund it.”

Founder Playbook: How to become a “must-buy” for a Mini-Strategic

At MarketCraft we help early-stage medtech companies engineer their markets — from attention to adoption — so they’re in the best position for acquisition.

We do this by creating leverage with investors, customers, and scaled strategics long before founders reach the negotiating table. Here’s what founders should be building into their go-to-market DNA:

1. Build the acquirer memo first

Before you write your pitch deck, write your two-page bolt-on brief.

Spell out your clinical endpoints, regulatory progress, reimbursement logic, and cost synergy model. This is the document that makes an acquirer’s BD team nod yes.

Think of it as market/product fit, not product/market fit.

You’re not waiting for a market to discover you — you’re engineering a market that sees your solution as inevitable. The earlier you define who you’re building for, the faster you’ll align validation, messaging, and valuation.

2. Engineer your pricing and reimbursement economics early

Pricing isn’t just about revenue — it’s how you signal market maturity and acquirer readiness.

A clean reimbursement path or scalable gross margin story doesn’t just win investors; it eliminates acquirer friction.

When your economics map cleanly into a strategic’s existing structure, you’re no longer pitching — you’re presenting an accretive asset.

This is Market Engineering as capital strategy: aligning your pricing architecture with how strategics underwrite value.

3. Treat Market Engineering as a capital strategy

Mini-Strategics don’t buy features — they buy engineered markets. They pay for narrative clarity, ecosystem momentum, and dominance of a defined space.

Category design out-defines competitors; Market Engineering out-competes them. The goal isn’t just awareness — it’s to make your position the gravitational center of the niche.

So define the phrase you want your acquirer to own (“The surgical wound intelligence platform,” “The hybrid neuro-navigation OS”), then own that word across your decks, data, and digital footprint.

As Bruce Cleveland writes: “Market Engineering is the CEO’s system design, not a marketing program.”It’s cross-functional — product, sales, finance, and story all moving in one engineered direction.

4. Build your early clinical pipeline — it’s your market signal system

Your first CRM isn’t for customers; it’s for market signal capture. Track every clinician, pilot site, and feedback touchpoint — this data becomes proof of traction and integration readiness.

Founders who can quantify early adoption signals — not just talk about them — engineer confidence in investors and acquirers alike.

Even two years out, you should be capturing data on every clinician, hospital, or pilot site that has expressed interest or engaged. Just use the free version of HubSpot — it will also automatically capture emails, and you can create a pipeline.

That simple pipeline becomes your leverage in investor and acquirer conversations, and later your roadmap for field deployment — showing where to hire reps, which regions are warming up fastest, and where early adoption is most likely to compound.

The data you track before launch shapes how efficiently you scale after it.

5. Use social as your market testbed

Forget vanity metrics. Use LinkedIn and founder-led storytelling as your market engineering lab — run messaging experiments, test positioning narratives, and identify which pain points generate institutional engagement.

Run narrative experiments, observe who engages, and refine how you frame the problem.

This isn’t vanity engagement — it’s narrative A/B testing in public. When strategics start echoing your language, you’ve succeeded. You’ve engineered market consensus.

Want to learn more? DM me directly — or my team on the MarketCraft LinkedIn page — to set up an analysis call.